In this Intel earnings call summary, we summarize key metrics and topics discussed on the Q2 2022 call, including:

- Earnings Call Summary

- Revenue Highlights

- Profitability

- Industry Trends

- New Initiatives

- Mergers & Acquisitions (M&A)

- Key Partnerships

- Upcoming Product Launches

- Guidance

- Caller Q&A

This earning call summary was done by our GPT-3 enabled earnings call assistant, which you can learn more about here.

Earnings Call Summary

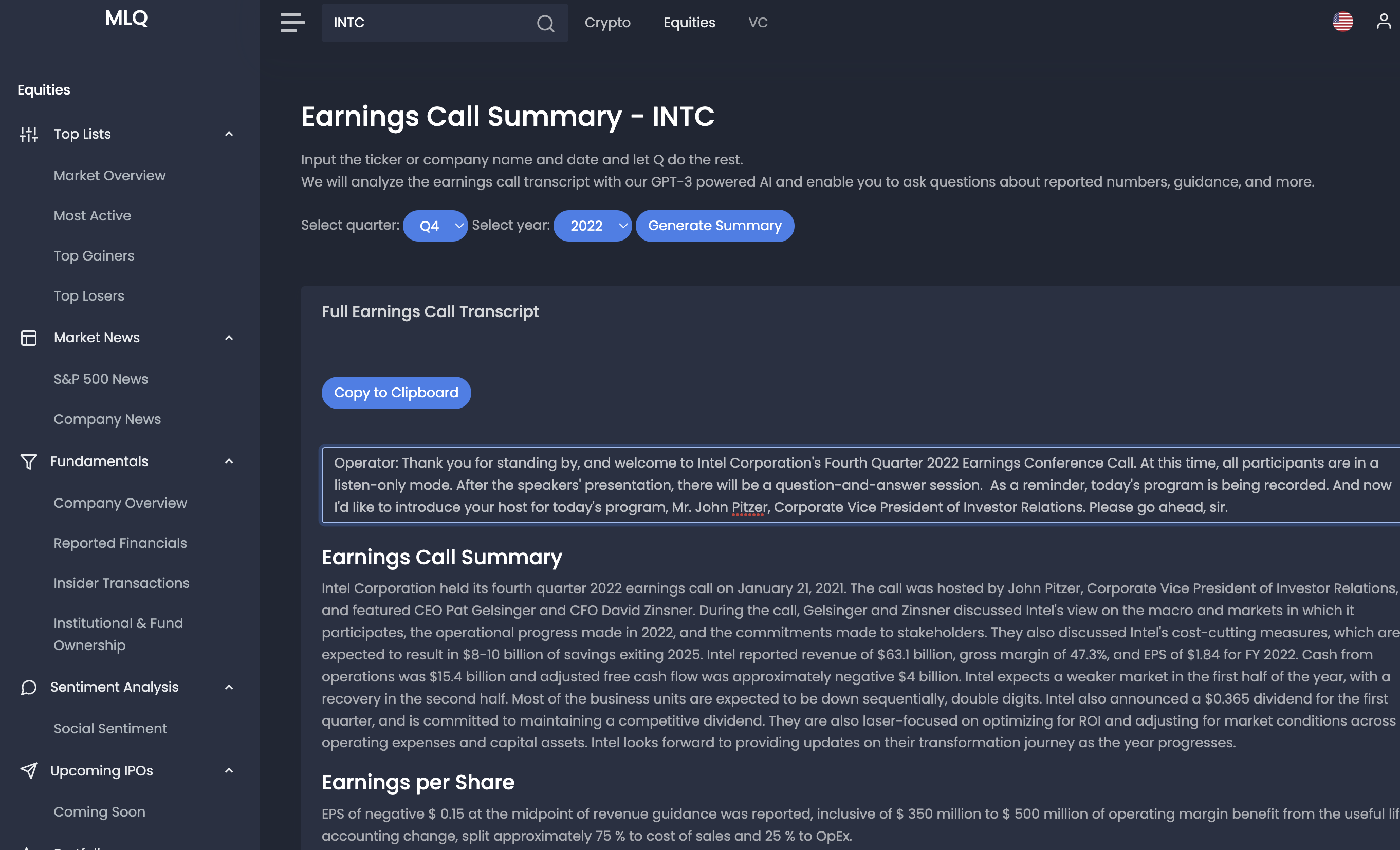

Intel Corporation held its fourth quarter 2022 earnings call on January 27, 2023. The call was hosted by John Pitzer, Corporate Vice President of Investor Relations, and featured CEO Pat Gelsinger and CFO David Zinsner.

During the call, Gelsinger and Zinsner discussed Intel's view on the macro and markets in which it participates, the operational progress made in 2022, and the commitments made to stakeholders.

They also discussed Intel's cost-cutting measures, which are expected to result in $8-10 billion of savings exiting 2025.

Intel reported revenue of $63.1 billion, gross margin of 47.3%, and EPS of $1.84 for FY 2022. Cash from operations was $15.4 billion and adjusted free cash flow was approximately negative $4 billion.

Intel expects a weaker market in the first half of the year, with a recovery in the second half. Most of the business units are expected to be down sequentially, double digits. Intel also announced a $0.365 dividend for the first quarter, and is committed to maintaining a competitive dividend.

They are also laser-focused on optimizing for ROI and adjusting for market conditions across operating expenses and capital assets. Intel looks forward to providing updates on their transformation journey as the year progresses.

Revenue Highlights

Fourth quarter revenue was $14 billion, landing at the low end of the range and down 8% sequentially. Revenue from DCAI and NEX were in line with expectations, while CCG revenue was $6.6 billion, a decline of 36% year-over-year as PC TAM deteriorated faster than expected due to macroeconomic headwinds. Customer inventory remains elevated beyond previous expectations and will continue to burn into the first half of 2023.

Intel 7 product mix also impacted DCAI revenue, which was down 33% year-over-year, driven by TAM contraction and competitive pressure. Despite the macro headwinds, Intel achieved record quarterly revenue of $319 million, up 87% sequentially and 30% year-over-year on increased automotive shipments.

Profitability

Intel reported a negative EPS of $0.15 at the midpoint of revenue guidance for the quarter. This was inclusive of $350 million to $500 million of operating margin benefit from the useful life accounting change. Factory underload charges impacted Q1 gross margin by 400 basis points. Intel reported a gross margin of 47.3% and EPS of $1.84 for the full year.

They generated $15.4 billion of cash from operations and an adjusted free cash flow of approximately negative $4 billion at the low end of the range they provided last quarter. Intel is forecasting a gross margin of 39% and a tax rate of 30% for the first quarter.

Industry Trends

This quarter, the semiconductor industry is facing a significant inventory correction cycle, with the first half of the year expected to be down year-on-year before returning to growth in the second half. This is being driven by macro uncertainty, rising interest rates, geopolitical tensions in Europe, and COVID impacts in Asia, especially in China.

The PC market has seen a further deterioration as we ended calendar year 2022, with the PC consumption TAM estimated to be between 270 million to 295 million units. Additionally, the networking space is expected to experience some softening, but not as much as other segments. Lastly, the installed base has gone up, giving reasonable confidence that post this period of inventory correction, the market will be healthy.

New Initiatives

This quarter, Intel announced a number of initiatives to improve gross margins and reduce costs. These initiatives included the Smart Capital Initiative, which was announced at the Analyst Day and is expected to provide a significant lift to gross margins.

Intel also announced a $3 billion spending reduction with significant austerity across the company, and a change in ending inventory values that will not be counted towards the $3 billion short-term or $8 billion to $10 billion long-term structural cost improvements.

Additionally, Intel is investing in manufacturing, design, products, and foundry to drive their transformation and create the flywheel for IBM 2.0. Lastly, Intel is investing in vPro in the enterprise market to help customers drive a return on investment.

Mergers & Acquistions (M&A)

Intel announced the acquisition of Tower Semiconductor in the fourth quarter of 2022. The acquisition is expected to amplify Intel's momentum in the foundry business and make it more attractive to customers. Intel also announced the acquisition of Habana Labs in the fourth quarter of 2022.

The acquisition is expected to strengthen Intel's AI capabilities and expand its portfolio of AI solutions. Intel also announced the acquisition of Moovit in the fourth quarter of 2022. The acquisition is expected to expand Intel's mobility solutions and help it better compete in the autonomous vehicle market. Intel is making strategic investments in M&A to position itself for long-term growth in a market expected to reach $1 trillion by 2030.

Key Partnerships

Intel has made significant progress in its partnerships this quarter. They have engaged with seven out of the ten largest foundry customers, and have 43 potential customers and ecosystem partner test chips.

Intel has also made progress on Intel 18A, and have shared the engineering release of PDK0.5 with their lead customers. Additionally, Intel is working hard to complete the Tower acquisition, which will further amplify their momentum as their foundry business becomes even more compelling to customers. Intel has also seen enthusiasm for their latest Alchemist-based discrete graphics products, and expect volume ramp throughout the year.

Upcoming Product Launches

During the call, it was discussed that the Sapphire Rapids product line had just been released and was getting a great response from customers. It was also mentioned that Emerald Rapids is looking very healthy for later this year, and Granite Rapids and Sierra Forest are looking very healthy for next year.

Additionally, Intel 18A was discussed, with the engineering release of PDK0.5 having been shared with lead customers and the final production release expected in the next few weeks. Finally, the Tower acquisition was mentioned, which is expected to further amplify the company's momentum.

Guidance

Intel provided guidance for the first quarter of 2023, expecting a sequential revenue decline and negative operating margin. They forecasted a gross margin of 39%, a tax rate of 30%, and EPS of negative $0.15 at the midpoint of revenue guidance.

They also mentioned that factory underload charges are projected to impact Q1 gross margin by 400 basis points. Intel also mentioned that they are expecting macro weakness to persist at least through the first half of the year, with the possibility of second half improvements. However, they are not providing revenue guidance beyond Q1 due to the uncertainty in the current environment.

As always, none of this is financial advice, do your own research, and see our full terms and conditions for more.